Australian Natural Gas - How Much Do We Have And How Long Will It Last ?

Posted by Big Gav in australia, exports, gas, gorgon, lng, natural gas, north west shelf, woodside

Last year I took a look at the question "Should Natural Gas Be Used To Power New Zealand ?", after reading an article from NZ PEPA executive John Pfahlert arguing that New Zealand should be building new gas fired power stations instead of trying to become carbon neutral, and concluded that this seemed a rather risky strategy - depending on continuing offshore exploration success.

The view of the Australian government and gas industry seems to be that our gas supplies are essentially unlimited, with the phrase "more than a century of supplies left" bandied about at every opportunity. x-Prime Minister John Howard used to dream of Australia becoming an "energy superpower", with a vastly expanded gas (LNG) export industry being a cornerstone of this vision, based on Western Australian LNG exports from offshore gas fields.

In the lead up to the Australian election last year, the APPEA (Australian Petroleum Production and Exploration Association) was also arguing that gas should be our fuel of choice for power generation as we transition away from coal to a clean energy future, an idea which received a limited amount of support from Labor during the campaign. Since the election, the APPEA has continued to promote the vision of a gas fuelled power industry, recommending that at least 70 per cent of new electricity generating stations constructed in Australia to be fuelled by natural gas by 2017 and maintaining that "Australia's vast reserves of clean, natural gas are the key to meeting the nation's energy needs while reducing greenhouse gas emissions and maintaining economic wellbeing".

New Energy Minister Martin Ferguson also views natural gas as the key to Australia's energy security for liquid fuels, in the form of gas to liquids (GTL - as well as its more environmentally unfriendly cousin, coal to liquids, or CTL) and compressed natural gas (CNG). The view that CNG is a way to reduce our consumption of foreign oil is quite a common one, judging by some of the comments made on TOD ANZ - and elsewhere - from time to time.

The thing that strikes me as being rather quaint, to put it mildly, is that we pay anywhere from about $8 billion to $25 billion to import the oil and we get a paltry $4 billion for the gas that we sell to overseas countries. It seems odd to me, especially given gas is a superior fuel for many, many purposes including the use in motor vehicles - Ollie Clark, Natural Gas Vehicle Association

Recently Western Australia has announced that it will build a new coal fired power station to meet growing energy demand, ruling out a natural gas fueled plant because of supply shortages. This situation which seems to be at odds with both the APPEA's recommendation and with the notion that we have so much natural gas that we can not only be a large LNG exporter but also use it to fuel both our power plants and our transportation system, along with more traditional domestic and industrial uses.

In this post I'll have a look at how much gas Australia has and how long it will last under a variety of scenarios - from an indefinite continuation of the current rate of production to a pell-mell conversion to use gas for all our energy needs combined with a rapid expansion of LNG exports.

Australian Natural Gas Reserves

Most of the data in this section was sourced from a paper published earlier this year by Mike Roarty of the Parliamentary Library research section on "Australia’s natural gas: issues and trends", and Brian Fleay's paper "Natural Gas, "Magic Pudding" or Depleting Resource" (pdf), which in turn used data from the Geoscience Australia "Oil & Gas Resources of Australia 2004" (pdf) report. Where newer information has been available I've linked to the source (more often than not either The Australian's Nigel Wilson or Bloomberg's Angela McDonald-Smith, who do the most comprehensive coverage of local energy news).

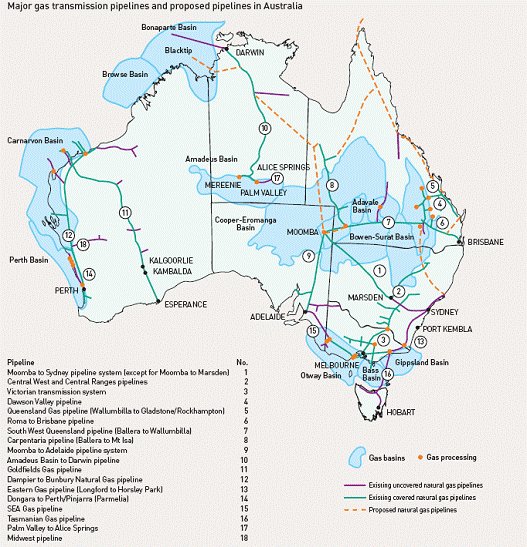

Cooper Basin - The largest onshore conventional gas reserves occur in the Cooper/Eromanga Basins in north-east South Australia and south-west Queensland. This source currently supplies much of the domestic eastern Australian gas market (South Australia, the Australian Capital Territory, New South Wales, and Queensland), but is mature and now depleting rapidly.

Bass Strait - Victoria and Tasmania are primarily supplied by the Gippsland Basin offshore from south east Victoria, with a newer development in the area, the Kipper field, expected to come online in 2011. There have also been new developments in the Bass and Otway Basins offshore south western Victoria - including the Yolla, Minerva, Casino, Geographe and Thylacine fields. In recent years, BHP have upgraded their estimated of Bass Strait gas reserves, with the Gippsland Basin thought to still contain around 7 tcf of gas.

The older fields in the south east are expected to have run down by 2020, but the newer developments in Bass Strait should extend that date out by another decade.

North West WA - Carnarvon and Browse Basins - Over 90 per cent of the reserves are located offshore from northwest Western Australia (Carnarvon and Browse Basins) and in the Timor Sea to the north of Australia (Bonaparte Basin) - far away from the primary domestic gas markets in the south east.

North West WA - Carnarvon and Browse Basins - Over 90 per cent of the reserves are located offshore from northwest Western Australia (Carnarvon and Browse Basins) and in the Timor Sea to the north of Australia (Bonaparte Basin) - far away from the primary domestic gas markets in the south east. The Carnarvon Basin is home to the existing North West Shelf gas fields - with the Gorgon / Jansz fields being the largest in the country. The area includes a number of fields supplying gas into the domestic gas network, particularly for use by the mining industry. Besides the existing North West Shelf gas project, other planned new LNG projects in the area include the Pluto (at the early stages of construction), Gorgon, Wheatstone and Scarborough fields.

The Browse Basin is the most active new frontier, with the area seeing successful exploration in recent years - reserves figure for Inpex's Ichthys field recently being upgraded by 3.3 tcf to 12.8 tcf of gas, for example. Woodside's planned Browse LNG development is also in this basin.

Northern Territory - Bonaparte Basin / Timor Sea - The area between the Northern Territory and East Timor is the other region currently producing significant amounts of gas (and oil) with an LNG plant recently starting operation in Darwin and other fields being considered for development.

The division of gas revenues from the region between East Timor and Australia has been the subject of a lot of controversy over the years, which has contributed to continuing delays in developing the Greater Sunrise field.

Papua New Guinea - For many years it appeared that a gas pipeline would be built between Papua New Guinea and Australia, enabling east coast gas markets to access the gas reserves held by PNG (estimates range from 14 tcf to 40 tcf). Hopes of this occurring were still flickering as recently as the beginning of the year, however Oil Search and ExxonMobil have now decided to develop an LNG plant instead, making any future pipeline project very unlikely.

How Much Gas Do We Have ?

As at 1 January 2005, Australia’s Category 1 and 2 reserves totalled around 144 trillion cubic feet (tcf), according to the Geoscience Australia report, a slight decline on the previous year.

According to the Financial Times (quoting PFC Energy), Australia has so far produced only about 15 per cent of its gas resources, compared with 25 per cent for Norway and more than 80 per cent for the US’s lower 48 onshore reserves. Whereas US production has peaked (and Norway’s is expected to peak within a matter of years) Australian production is expected to expand until 2030.

| Basin | Reserves (2005) |

| Carnarvon | 80.6 tcf |

| Browse | 33 tcf |

| Bonaparte | 22.9 tcf |

| Gippsland | 7 tcf |

| Otway | 2.4 tcf |

| Cooper/ Eromanga | 1.9 tcf |

| Others | 2.5 tcf |

| Total | 150 tcf |

The table above has been adjusted to include the reserves revisions I've noticed since 2005 - Gippsland Basin from 3.1 to 7 tcf and Browse Basin from 30 tcf to 33 tcf (if you know of any others, please leave a comment).

Since then, based on an annual consumption rate of around 1.8 tcf, we have consumed around 5.4 tcf of gas, which would bring the current reserves number back down to around 144 tcf.

To put the Australian figure in context, proven world gas reserves are estimated to be over 6200 tcf - Australia has around 1.4% of the total.

How do we use the gas ?

In the domestic market, gas is primarily used for :

1. Manufacturing (36% of the total) - smelting, fertilisers, plastics and glass/brick/cement production

2. Power generation (32%)

3. Mining (13%)

4. Residential use (12%) - water heating, space heating and cooking

Obviously these will be joined by transportation if Mr Ferguson's plans for GTL/CNG are put into practice, and power generation will increase in importance if the APPEA's suggestions are implemented.

The fertiliser industry is an interesting one - globally the industry seems to be migrating towards natural gas supplies, particularly in the middle east, but also to Western Australia, where the Burrup plant now produces around 6% of the world's tradeable ammonia.

The rest of our gas goes to the export market, in the form of LNG (plus some condensate).

At present, there are 2 LNG plants in operation - the North West Shelf gas project (operated by Woodside Energy) near Karratha in WA, and the ConocoPhillips Darwin LNG plant in the Northern Territory. The North West Shelf project is the third largest LNG exporter in the world, with its fifth LNG train due to commence operation this year, bringing the capacity of the plant to 16.3 million tonnes (0.85 tcf).

A number of other projects are underway, in planning or actively under consideration - the table below lists all Australian LNG projects (using conventional gas).

| Project | Operator | Location | Yearly Capacity | Fields | Start Date (Est) |

| North West Shelf | Woodside | Karratha, WA | 0.85 tcf | 22 tcf | Existing |

| Bayu Undan | ConocoPhillips | Darwin, NT | 0.17 tcf | 4 tcf | Existing |

| Pluto | Woodside | Karratha, WA | 0.22 tcf | 5 tcf | 2010 |

| Browse | Woodside | TBD | 0.5 tcf | 18 tcf | 2015 |

| Gorgon | Chevron | Barrow Island | 0.8 tcf | 40 tcf | 2012 |

| Ichthys | Inpex | Kimberly (TBD) | 0.3 tcf | 12.8 tcf | 2013 |

| Sunrise | Woodside | Floating | 0.26 tcf | 9 tcf | 2015 |

| Scarborough | BHP Billiton | Floating | 0.3 tcf | 11 tcf | 2015 |

| Wheatstone | Chevron | Karratha | 0.24 tcf | 4.5 tcf | TBD |

| Evans Shoal | MEO Australia | Tassie Shoal | 0.13 tcf | 6.6 tcf | TBD |

| Total | 3.7 tcf | 132 tcf |

Australian LNG exports currently rank in the top 3 globally, however looking at new projects around the world, you can see that Australia's LNG exports will shrink in importance as projects in Qatar, Iran and Russia, in particular, start to deliver large volumes of LNG.

Political Factors

As I noted in the preamble, Western Australia recently opted to build a new coal fired power station instead of using gas as originally planned, due to the shortage of gas in the south of the state.

The WA domestic gas shortage has resulted in a local pressure group called the "DomGas Alliance" being formed to try and force the oil and gas companies holding offshore leases to either develop the fields or relinquish the leases - a move the APPEA oddly claims would "discourage exploration".

Martin Ferguson has also backed the "use it or lose it" idea, though he has apparently already been called in for a "quiet chiding" over this issue by the APPEA.

The APPEA is also unhappy about the state passing a law to force developers of LNG plants to set aside 15% of their reserves for domestic consumption, which is the only sign of the Export Land Model making any form of appearance for Australian energy production - and a pretty feeble one at that.

A planned expansion of the pipeline from Dampier to Bunbury should partly alleviate the gas supply issue by 2010, though in the short term an explosion at Apache Energy's Varanus Island plant has left the state gasping for gas, particularly the mining industry. This outage is expected to take months to repair.

One interesting side effect of the WA law is that BHP is considering building a floating LNG plant for the Scarborough and Thebe fields, partly to avoid these sorts of regulations.

Woodside have also been considering a floating platform for the greater Sunrise project, again in part to avoid any political risks associated with a plant in East Timor.

The only other form of notable state government intervention in the sector is the Queensland government's "smart energy policy" which mandates that 18% of power consumed in the state come from gas by 2020 (up from the earlier 13% target).

The recent federal budget eliminated a tax break for condensate production by the North West Shelf venture, prompting an expression of annoyance from Woodside CEO Don Voelte. At the time it was rumoured the industry would probably see the money returned via incentives for GTL production or faster development of LNG projects.

This has duly happened, with Ferguson kicking off a review of the tax system by Treasury secretary Ken Henry that will "include an assessment of the barriers to investment in large-scale downstream gas processing projects in Australia, the particular hurdles faced by remote gas developers, and consideration of the future policy framework for new sunrise industry development in the gas sector, including new LNG, gas-to-liquids and domestic gas projects".

The point of tax breaks isn't clear to me, given that the primary constraints on development of LNG projects in Australia are firstly finding a customer who will sign up for a long term supply deal and secondly availability of skilled labour and service companies - neither of which will be altered in the slightest.

It may perhaps encourage the development of a GTL project which might otherwise be unviable as a standalone LNG project though, such as Wheatstone.

The most obvious impact of the LNG export industry on the local gas market has been to push gas prices up, as the market is exposed to international supply and demand forces rather than purely local ones. Western Australia has already seen this (Santos CEO David Knox saying prices are headed for "LNG parity") and the same thing seems likely to occur on the east coast.

Another impact of the LNG export industry is that it will further increase the nation's dependence on income from fossil fuel exports.

Coal is currently our major export earner, which has prompted concern about Australia suffering from what is known as "The Dutch Disease" - the theory that an increase in revenues from natural resources will deindustrialise a nation’s economy by raising the exchange rate, which makes the manufacturing sector less competitive. The term was coined in 1977 by The Economist to describe the decline of the manufacturing sector in the Netherlands after the discovery of natural gas in the 1960s.

With the value of gas exports likely to rise to a similar level to that of coal if all the planned LNG projects go ahead, we could see more than a quarter of national GNP coming from these 2 industries.

How long will the gas last ?

According to the Parliamentary Library report, our resources are "capable of sustaining our future production and exports well into and probably throughout the 21st Century". While the paper was published on April 1, it appears to be serious.

Australia’s natural gas consumption for 2005–2006 amounted to 1,184 PJ. Additionally, exports in that year were 12.5 million tonnes (Mt) of LNG equivalent to 685 PJ - a total of 1,869 PJ (equivalent to around 1.77 tcf). Given the reserves and resources figure quoted of 144 tcf, this would mean our gas supplies would last for 81 years at the current rate of consumption.

One complicating factor is the use of biogas. According to the ESAA renewable sources of gas (primarily landfill gas) comprise about 16 per cent of Australia’s domestic gas use - which would equate to around 189 PJ (or 0.18 tcf).

Taking this into account, supplies under this simplistic scenario would last around 90 years - roughly the "end of the century" timeframe mentioned in the Parliamentary Library report.

Of course, neither domestic consumption nor exports are expected to remain static, so let's consider a few additional scenarios.

Note - as these scenarios are just examples, I haven't been particularly rigorous in running the numbers - they should be accurate to within 5% or so. Please bear this in mind if you feel the urge to nitpick - however if you can see any gross errors in the calculations please feel free to derive some alternate figures and explain them in the comments - its entirely possible the conversion factors have gone badly awry in the more complicated scenarios.

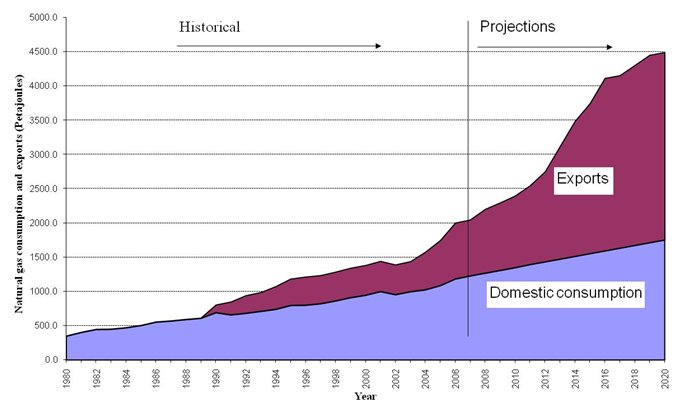

Scenario 1 - Increasing domestic demand and exports until 2020, remaining stable thereafter

The figure above shows the forecast growth in production from ABARE and the ESAA - continuing growth in domestic gas use and a sizeable expansion of LNG export capacity. By 2020, production is expected to reach 4500 PJ per year (or 4.3 tcf).

Allowing for biogas production at the same rate as today, this would mean natural gas supplies would last until 2046 - approximately 38 years.

Scenario 2 - Increasing domestic demand to 2030, static LNG exports from 2020

If domestic gas use continues to expand at the rate shown above, we'd expect to be using 2000 PJ per year for domestic purposes. Assuming no new LNG plants are built after 2020, we would be producing almost 5000 PJ per year (or 4.75 tcf).

Again, allowing for biogas production at the same rate as today, this would mean natural gas supplies would last until 2044 - approximately 36 years.

Scenario 3 - Increasing domestic demand and exports until 2020 (then stable), GTL/CNG for all transportation from 2020

As our energy minister is a strong advocate of using gas for transportation, it is worthwhile considering what would happen if the vehicle fleet was switched over to use CNG and GTL products, combined with scenario 1 for domestic use and exports.

Kiashu was kind enough to try and work out how much gas it would take to replace our current consumption of petrol and diesel, and came up with this set of calculations:

Petrol usually has about 34.6MJ per litre. Natural gas here in Australia is 38.87MJ per cubic metre at atmospheric pressure. Both vary a bit, obviously, but we can use this for some guesstimates. So we see that 1lt petrol is equivalent in energy to 34.6/38.87 = 0.89m3 natural gas.

An ABS survey [pdf- http://www.ausstats.abs.gov.au/ausstats/subscriber.nsf/0/12594B5543CA578CCA2571E2001C705D/$File/9208055005_2006.pdf] tells us that petrol use is a bit uncertain, figures are within about 10% only, but nowadays it's about 20Glt annually [numbered pp78, pdf p13-14].

20Glt petrol is equivalent in energy to 17.8 Gm3 of natural gas.

However, the natural gas must be compressed to 200-220 atmospheres - call it 210. As with the air car, this takes energy. The energy E required to compress air at 25C is,

E = 110,000 x ln (P1/P2) /m3/mol

There are 44.74 moles of methane in 1m3 of natural gas - natural gas is usually about 95% methane, and 5% carbon dioxide, propane, butane, sulphides and so on. Let's assume it's all methane to save ourselves the headaches. We're compressing it to 210 times atmospheric pressure, so P1=210 and P2=1, so the energy required to compress 1m3 of natural gas into CNG will be,

E = 110,000 x ln (210) = 588,181J = 0.59MJ

0.59MJ is 0.59/38.87 = 1.5% of the energy of the natural gas. So turning NG into CNG uses 1.5% of the energy content. Put the other way, you only get 98.5% of the energy from CNG you would from burning NG directly. Thus, 20Glt petrol is equivalent, after compression of NG into CNG, to 18.07Gm3 of NG (not a typo - we don't care about the volume of the CNG, only the NG feedstock)

I don't know about CNG efficiency compared to petrol and diesel. If that's lower or higher it'll obviously affect how much natural gas we need. But we can say that a figure somewhere on the cricket pitch is 18 billion cubic metres of natural gas to replace the 20Glt of petrol we use these days. ...

Hmmm, actually the ABS here says that in 2006 total fuel use was 16.3Glt petrol + 5.74Glt diesel = 22Glt. Must be more than 22Glt by now... but you can take the conversion factor of lt petrol ---> m3 natural gas of 100% --> 90% as being about right. For every 1Glt fuel you replace you want 900M m3 of natural gas.

By my calculations, 900 million m3 of gas equates to 32 billion cubic feet of gas (or 0.032 tcf). So for 22 Glt of fuel, we are looking at 0.7 tcf of gas per year for the present day vehicle fleet.

If we assume the fuel consumption of the national vehicle fleet remains static, and it suddenly switches from petrol and diesel to CNG/GTL in 2020, we'd be consuming 5 tcf per year minus biogas.

This means natural gas supplies would last until 2042 - approximately 34 years (ie. the new gas powered vehicle fleet could be used for just over 20 years before we had to junk it and replace it with electric transportation).

Scenario 4 - Increasing domestic demand and exports until 2020 (then stable), domestic gas use for all new power generation

As noted in the preamble, the APPEA is keen for us to transition to cleaner energy source by using gas for power generation until we get finally around to replacing coal (the dominant source at present) with renewable energy sources.

Doing the numbers (with some input from kiashu again), natural gas contains around 38.8MJ/m3, or 10.78Kwh. Our natural gas reserves of 144 tcf (4077 billion cubic metres) could therefore generate 43,950 billion Kwh (or 3.26 tcf per trillion Kwh) - at 100% efficiency.

Modern natural gas plants manage around 55% efficiency in the turbines, so if we allow for another 5% loss in the system we'll end up with about 23,000 billion Kwh (or 6.26 tcf per trillion Kwh).

National electricity generation in 2006 was 255 billion Kwh. Historically, electricity generation has been increasing at around 3% pa.

Assuming that we generate all new power from gas, natural gas supplies would last until 2043 - approximately 35 years (ie. the new - and old - gas fired generation capacity could be used for just over 30 years before we had to junk it and replace it with renewables as well).

Conclusion

There are a myriad of scenarios that could be applied (try working out one where the export land model applies to our gas exports for example, which would increase the timeframes somewhat, or one where exports keep increasing after 2020, which would significantly decrease the timeframes), but I think its safe to assume that if we start treating natural gas as a silver bullet we will run out in less than 40 years - with gas fired power for new generation being much less intensive in its use of gas than using GTL/CNG for transport.

The X Factors - What Other Sources Of Gas Do We Have ?

In the scenarios outlined above I've used our current known gas reserves as the total supply available.

There are a number of ways of further increasing (or extending the use of) our gas supplies :

1. "Just find more"

Martin Ferguson's preferred approach to oil and gas depletion is apparently to "just find more". This isn't totally out of the question of course - the recent expansion of "Australia" to include all of the continental shelf (see pdf map here) will no doubt include more oil and gas - but how many more years worth is an open question.

The APPEA argues that Australia has 50 sedimentary basins, of which just 12 are producing oil and gas (4 basins have been deemed non-commercial) and that there is still potential for drilling in little explored areas.

How much potential there is depends on your view of exploration programs. If you think that exploration is now a well understood science, and that companies target the most likely areas when exploring, then you'd assume that there isn't a great deal of gas left to be found.

If, on the other hand, you think that exploration is similar to roulette (the cynical view), or that governments and oil companies wish to restrain discovery and production (the conspiratorial view) then there may be much more - maybe twice as much as has currently been discovered.

The safest assumption to make is the first one.

2. Efficiency improvements

There are some obvious areas of improvement that could be made to reduce gas usage on the power generation and domestic use front. A number concentrated solar thermal plants under construction are combined with gas fired power to reduce total gas consumption (though obviously the long term direction for these plants is to burn no fossil fuels at all).

Another mechanism for improving the efficiency of gas usage in power generation is cogeneration (capturing energy from waste heat, which is already done by some large scale industrial users, is another useful technique).

Usage of gas in plastic production could be reduced in some cases by producing bioplastic instead.

Finally, usage of gas for water heating could be reduced or even eliminated using solar hot water heaters.

3. Biogas

As noted earlier, biogas is already providing a proportion of our gas production. Getting a handle on just how much gas could be produced from biomass is quite difficult, but if you consider that methane from waste bananas alone could power a town of around 25,000 people, there is obviously quite a lot of potential. If you read the preceding link you'll see that the German Greens have proposed some incredibly ambitious targets for biogas production in Europe, so it is conceivable that biogas could provide a significant proportion of our energy needs.

Of course, if we produce enough, someone may decide to start turning it into LNG and shipping it offshore, so this wouldn't necessarily be a panacea.

3. "Unconventional" gas sources, Coal Seam Methane and Shale Gas

The real X-factor for gas production in Australia is unconventional gas sources, in particular coal seam methane and gas from shale. As both coal and shale are plentiful (and likely to remain so for some time), these are likely to provide significant quantities of gas.

The real X-factor for gas production in Australia is unconventional gas sources, in particular coal seam methane and gas from shale. As both coal and shale are plentiful (and likely to remain so for some time), these are likely to provide significant quantities of gas.No one seems to be attempting to extract gas from shale in Australia at this point in time, so I won't attempt to quantify how much gas we could possibly obtain from this source (see this post for a discussion of unconventional gas, including from shale, in the US).

Coal seam methane, on the other hand, is now the focus of a boom in Queensland. As there has been so much activity in the area lately (and reserves numbers are so vague) I'll make this the subject of a separate post - and re-run the scenarios based on various estimates of CSM potential.